Edited by Vinay Pandya

Markets are in upheaval and volatile due to high degree of speculation and recent rate hikes by various Central Banks. However, we need to ponder and think about: Will they go up TOO much or cannot be moved up during structural issues? Let’s examine the factors:

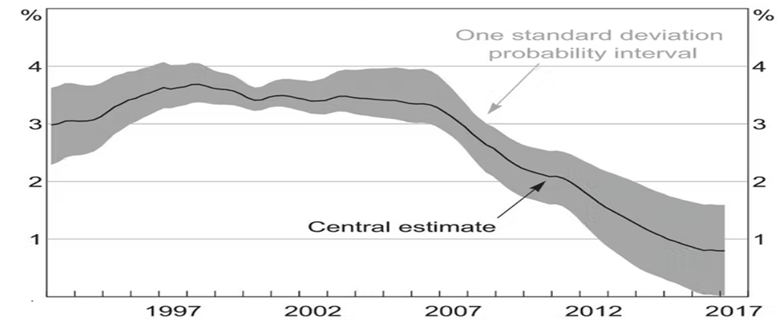

The neutral rate is usually described as the real (inflation-adjusted) interest rate that is either expansionary or contractionary, (pushing up inflation and unemployment). More crucially, the neutral rate should be one that, over time, matches the total supply of savings with the total demand for those savings by enterprises and people seeking to put them to use in the construction of structures and equipment (capital investment).

The neutral rate of interest has been declining for 40 years, as Treasury Secretary Stephen Kennedy noted in this year’s post-budget address. They have now turned Negative. So, an increase is a mere attempt to reduce the negative bias. This indicates that the bank believes the actual (inflation adjusted) neutral cash rate is -2%.

Neutral Interest Rate Estimates:

Source: RBI

Inflation is the key – We are already seeing serious inflation pressures and price rises. This, however, could be a transitory effect, as economies will enter recovery with large spare capacity, notably in the labour market. For a temporary increase in prices to become a sustained acceleration in inflation, salaries would have to rise, putting further cost pressure on prices. With unemployment substantially above global equilibrium estimates, this seems implausible. The unemployment rate in the United States is currently at 6.7 percent, significantly above the equilibrium rate. While the link between unemployment and wages has diminished in recent years, workers will continue to face deflationary pressure on salaries for some time as they compete for jobs.

Source: Schroders

There is uncertainty about how the extra liquidity created during the crisis will be spent, as well as how Covid’s long-term impacts may alter equilibrium unemployment. Either scenario could result in higher costs due to increased global demand or decreased supply. Higher sustained inflation remains a concern.

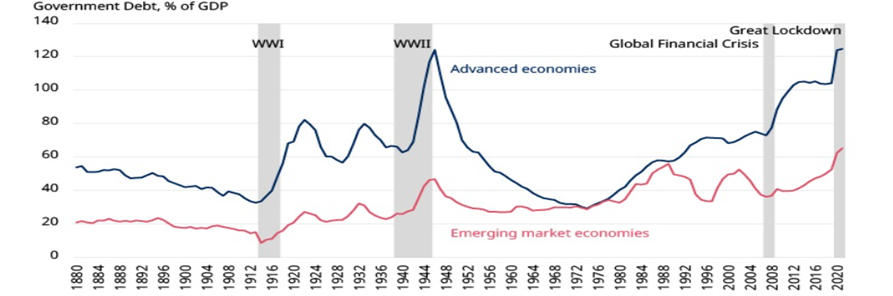

The degree of debt in the global economy is one explanation for this. According to IMF figures, government debt in major economies has reached levels not seen since World War II.

High government debt levels will reinforce low rates – While some regard high debt as a sign of rising inflation, believing that the government will attempt and succeed in depreciating its liabilities through inflation, this has not been the case in Japan. In Japan, high debt has hampered growth by limiting the government’s capacity to adopt flexible fiscal policy to support growth. Meanwhile, large levels of private sector debt have hampered monetary policy effectiveness by decreasing the appetite to take on further debt. Monetary and fiscal policy are both exhausted.

Source: IMF

Others are following suit. Policy rates are near zero, the banking system is receiving significant support through targeted refinancing, and the central bank is buying large amounts of assets. Although interest rates in the United States and the United Kingdom remain positive, monetary policy has been less effective in the actual economy since the financial crisis.

Looking ahead, with debt in both the US and the UK approaching 100% of GDP and both countries facing huge healthcare liabilities, fiscal flexibility will become more constrained. The pressure on central banks to keep rates low will continue high in this scenario. Not only to keep overall policy stimulative, but also to keep high debt levels manageable. In this regard, the Fed will resemble its Japanese counterpart, where low interest rates are critical to keeping government debt on a sustainable path.

As the global economy improves, central banks will keep policy lax in order to boost inflation and permit huge budget deficits and debt. We are living in unusual circumstances, but low interest rates are likely to stay even after the global economy has recovered from the pandemic. As investors chase profits in “the zero” environment, such an outlook will likely accelerate the demand for yield, resulting in volatility and bubbles.