Compiled by Khushi Tekwani

India is considered to be the fastest growing economy in the world. It is the world’s fifth-largest economy by nominal GDP and the third-largest by purchasing power parity (PPP). India’s economy has seen some major fluctuations in the last 5 years.

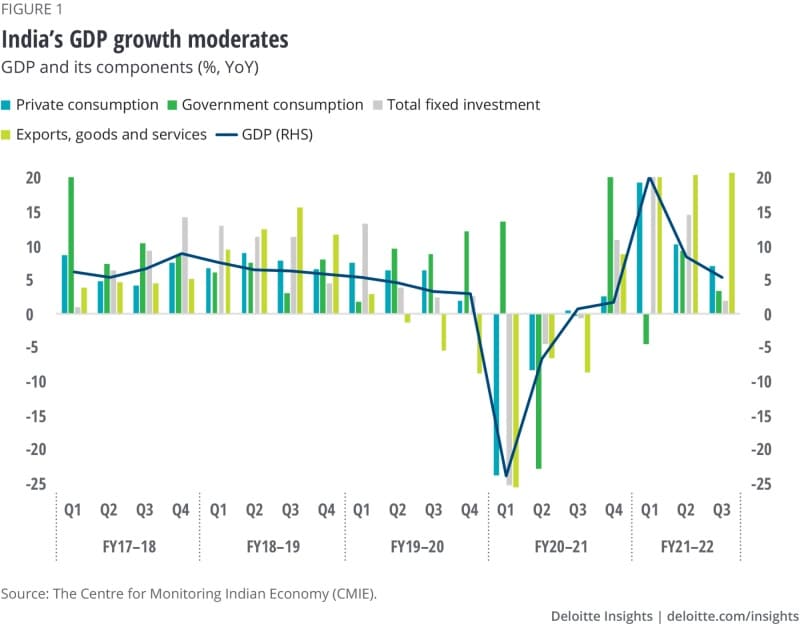

While the Covid crisis had impacted the economy in the initial state that led to the overall contraction in GDP of 7.3% for the FY 2020-21, which is the worst year in terms of economic contraction in the country’s history. In the subsequent year, economic activity rebounded strongly as India’s vaccination rollout accelerated. Furthermore, the elimination of containment measures, the ability of exporters to take advantage of favorable external conditions, and government support to vulnerable households combined to produce remarkably high GDP growth of 8.7% in FY 2021-22, that is above the pre-pandemic level.

Source: Deloitte Insights

Current Status:

- India’s nominal gross domestic product (GDP) at current prices is estimated to be at Rs. 232.15 trillion (US$ 3.12 trillion) in FY22.

- India is the third-largest unicorn base in the world with over 100 unicorns with a total valuation of US$ 332.7 billion.

- According to data from the Department of Economic Affairs, as of January 28, 2022, foreign exchange reserves in India reached the US$ 634.287 billion mark.

Factors contributing to the economic growth:

The growth-enhancing policies and schemes, like production-linked incentives (PLI) and the government’s push toward self-reliance and increased infrastructure spending, will begin to take effect in 2023, resulting in a stronger multiplier effect on jobs and income, increased productivity and efficiency, and accelerated economic growth. Specifically, the strengthened health infrastructure accompanied by roll out of Pradhan Mantri Garib Kalyan Yojana (PMGKY) and Atmanirbhar Bharat (ANB) packages that besides saving lives also protects livelihoods and businesses have also accelerated GDP growth.

There is a renewable-energy investment spree: India ranks third for solar installations and is pioneering green hydrogen. After the introduction of the Covid-19 virus, firms everywhere are attempting to reconfigure supply chains to lessen their reliance on China, and so, India’s attractions as a manufacturing location have risen, supported by helped by a $26bn subsidy scheme & government incentives such as lower taxes, and improved services exports on the basis of a greater global push toward digitisation and technological adaptation.

Challenges:

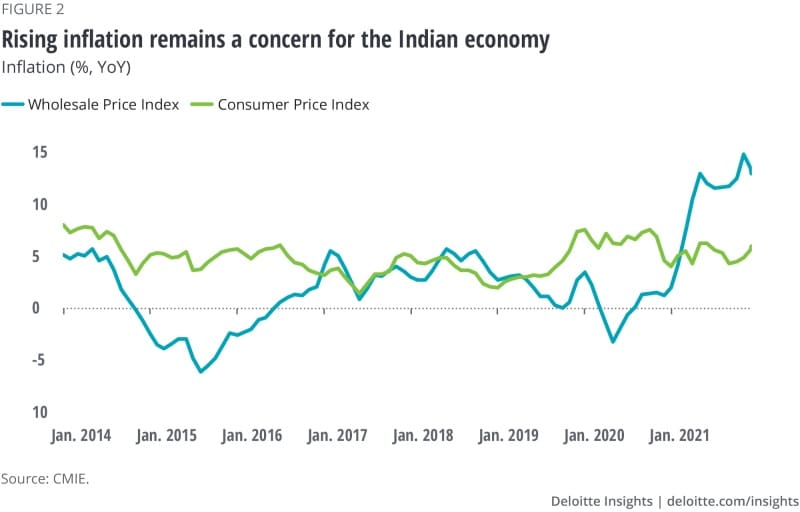

Right when the global economy seemed to be at the cusp of witnessing green shoots of recovery after the COVID-19 pandemic, the Russia-Ukraine crisis escalated. The crisis has clouded India’s growth outlook. Consequently, prices of crude oil and gas, food grains such as wheat and corn, and several other commodities have shot up. This rise in prices has pushed WPI or wholesale price-based inflation to a record high of 15.08 per cent in April and retail inflation to a near eight-year high of 7.79 per cent.

Higher fuel and fertilizer prices will reduce government revenues and increase subsidy costs. Furthermore, capital outflows and rising import bills will weigh on the current account balance and currency valuation.

Source: Deloitte Insights

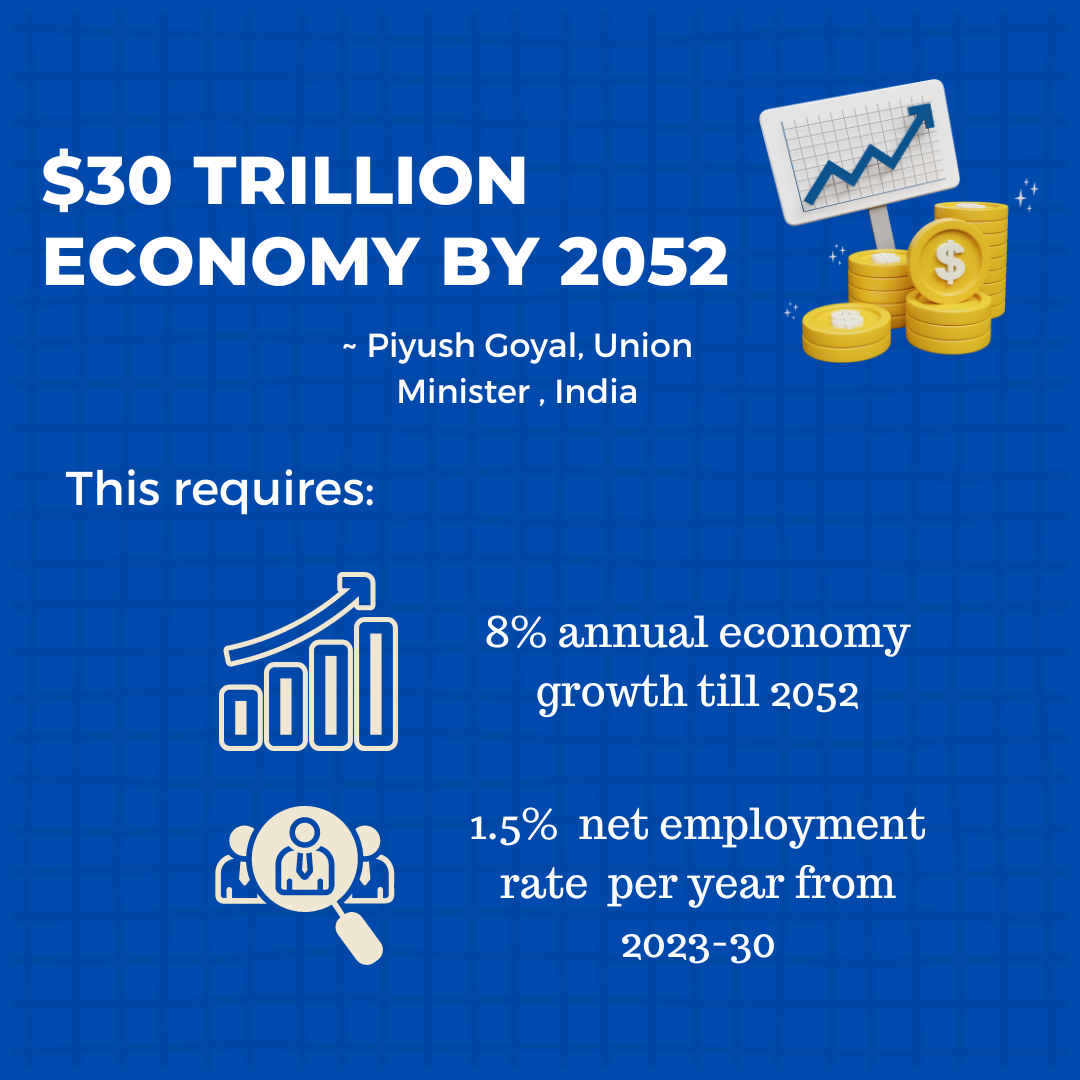

According to the union minister Piyush Goyal, India would reach the $30 trillion economy mark by 2052 from the current level of 3 trillion economy. Analytically, for this India needs to grow at 8 per cent every year on a compounded annual growth basis which has been debated since the announcement. While the World Bank cut India’s economic growth forecast for the FY 2022-23 to 7.5% as rising inflation, supply chain disruptions and geopolitical tensions taper recovery, a McKinsey Global Institute report opposed it and stated that “India needs to increase its rate of employment growth and create 90 million non-farm jobs between 2023 and 2030s, for productivity and economic growth. The net employment rate needs to grow by 1.5% per year from 2023 to 2030 to achieve 8-8.5% GDP growth between 2023 and 2030.”

Furthermore, India is focusing on renewable sources to generate energy. It is planning to achieve 40% of its energy from non-fossil sources by 2030. India is expected to be the third-largest consumer economy as its consumption may triple to US$ 4 trillion by 2025, owing to a shift in consumer behavior and expenditure pattern, according to a Boston Consulting Group (BCG) report. It is estimated to surpass the USA to become the second-largest economy in terms of purchasing power parity (PPP) by 2040, as per a report by PricewaterhouseCoopers. PPP is the macroeconomic analysis metric used to compare economic productivity and standard of living between the countries. It’s a theoretical exchange rate that allows companies to buy the same amounts of goods and services in any country.

The Indian economy has seen many ups and downs due to various challenges, be it religious, economic or political. Despite all of that, it has grown tremendously since independence at a very idealistic rate and could continue to do so if operated using the correct metric and statistics.